In the outskirts of Kapasia, 58-year-old Aamir (name changed) lives with his wife, mother, and two children. A participant in Hrishipara daily diaries research since 2015, Aamir holds a secondary school certificate (Grade 10) and was inspired by his mother to open his own retail shop. His daily records offer a window into how a micro-entrepreneur balances the pressures of daily survival and long-term asset building.

Household Earnings

Aamir’s shop earned a cumulative revenue of BDT 17.7 million over the past five years. Although this figure seems impressive, the analysis of his daily business operations reveals constant liquidity pressure. Each morning, he invests 8,000-12,000 Taka in buying stock, which almost covers his average daily sales of 10,000 Taka. This daily capital reinvestment leaves a thin profit margin, just enough to sustain his household needs while keeping his shop running. To further illustrate his business financials, the following table shows the total revenue and stock purchases over 5 years.

From 2021 to 2025, revenue grew from BDT 2.48 million to BDT 4.35 million, a 75% increase. However, profitability did not improve as stock purchases increased proportionally, leaving the profit margin at 5.4%-5.5%.

To maintain the household’s financial stability, Aamir’s mother engaged in livestock farming and sold them during festive seasons. The livestock sales generated a substantial 187% gross margin and a net profit of BDT 105,000, though such returns were infrequent. The resulting paradox was notable; while the retail shop accounted for 99% of total revenue, it yielded low margins; conversely, livestock farming offered high profitability but lacked the volume and consistency of the shop.

"Baki" (Shop Credit)

Another key finding from the qualitative interview is the prevalence of ‘baki’, a system where customers buy groceries on credit and pay in installments. This practice created a significant financial burden for Aamir. His outstanding ‘baki’ has now reached nearly BDT 100,000. He keeps a record and hopes to recover most of it, but some is unrecoverable as customers have migrated out of the area. With a tight 5% profit margin, he has reduced the amount of shop credit he gives over time, as it affects both his business and household stability.

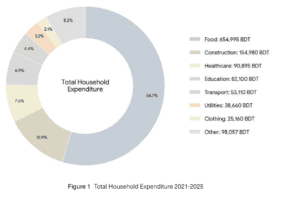

Household Consumption

Amid business pressures, household consumption patterns stayed consistent. Among non-business expenses, food (54.7%) accounted for the largest share of total household spending, followed by construction, health care, and education. Monthly cash flow fell short at times, especially when inventory purchases or payment cycles exceeded sales revenue.

Regular Savings

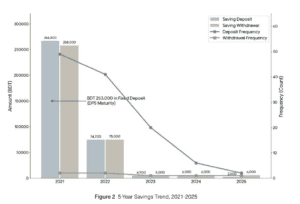

Aamir regularly saved in a Deposit Pension Scheme (DPS) at a commercial bank and a co-operative bank. His DPS matured into a significant lump sum in 2021, which he reinvested into a fixed deposit. However, over the last five years, his liquid savings have considerably decreased due to rising household expenses, including the medical costs of his father’s terminal illness and his children’s education. Figure 2 depicts five years of savings deposits and withdrawals, with transaction amounts shown as bars and frequencies as lines.

"Howlat" (Interest—Free Loans)

Aamir is cautious with debt. Over the last five years, Aamir’s total borrowing was BDT 250,000, equal to just 1.4% of his total revenue. This sum comprised two loans from a close relative: BDT 150,000 in September 2022 and BDT 100,000 in March 2023. Both loans were secured through “howlat”, a community-based, interest-free lending built on social relationships and trust.

Despite the high availability of microfinance loans in Bangladesh, Aamir avoided them, fearing that his thin profit margins and rising household costs would make repayments difficult to manage. He preferred informal loans over institutional ones, as they offered greater repayment flexibility. Notably, he never used debt for consumption and invested all borrowed funds in building long-term assets, such as buying property, renovating his house, and expanding his shop.

Conclusion

Aamir’s journey highlights the struggle to sustain a micro business amid market competition and rising household needs. Despite a 75% increase in revenue, his profit margins remained stagnant, highlighting a stark contrast between sales growth and profitability. Rising stock costs and the burden of ‘baki’ (shop credit) drained his liquidity; consequently, his high sales figures did not bring the financial ease due to tight cash flow.

In the midst of these challenges, Aamir manages his limited resources with care. To stabilize income, he leverages livestock sales, turns savings into secure fixed deposits, and uses ‘howlats’ (informal, interest-free loans). Even when family needs outpaced his retail earnings over the years, he maintained minimal withdrawals from his savings. His ability to buy land and expand his shop despite these constraints demonstrates his resilience in building household assets.

Aamir’s story makes it evident that meaningful growth for micro-businesses takes a long time to materialize; yet, it is the small choices, such as income diversification, affordable debt, and consistent saving, that ensure their survival. To move beyond mere survival, shopkeepers like Aamir could transition from the limitations of daily, cash-dependent buying to the more efficient bulk stock procurement. Such an approach, whether using informal or formal loans, would significantly reduce procurement costs and enable retailers to break the cycle of daily purchases, converting high sales volumes into sustainable profit margins.

written by Mercyline