If we look back at the history of accounting, it has been changing and improving constantly since its birth, and the scope it is covering is spreading and adapting with the ever-changing world of business. Accounting began as a book keeping approach by a merchant in Italy, but now it is used to account for the activities of most companies, with the main purpose of the investors’ protection. Now it is the time to move to the next stage as the nature of capitalism and business is to transform to the next phase. In my view, the key theme of the next phase is impact. For decades, the focus has been the company’s gains or losses. Now it will have to shift to the impact companies have on society, environments, employees, etc, which is a broader scope than ever.

1. History of Accounting

Accounting has gone through several evolutionary steps over the centuries:

- The 15th Century: Accounting first started in Italy, where the business was most thriving in the world at that time, by merchants who traded spices imported from Asia to export to the European countries and banks who were supporting them to record huge numbers of business transactions. (Accounting for Individuals)

- The 17th Century in the Netherlands: the Dutch East India Company was first established as a joint-stock company for the purpose of fundraising from anyone. To account for the profit and to equally distribute it to the investors, book-keeping of the company was required. (Accounting for Companies)

- The 19th Century in the UK: following the invention of the steam locomotive, companies began feeling the need for large upfront capital investment. To satisfy that need and stabilize the profits, they invented the depreciation mechanism. (Cash Basis to Profit Basis Accounting)

- The 20th Century in the USA: To respond to the 1929 great depression, the Generally Accepted Accounting Principles (“GAAP”) were developed in 1933 with the main purpose of protecting investors. (Disclosure / Accounting for Investors Protection)

What’s next then?

2. The 21th Century: Accounts for Impacts

Below is a mission statement published by Havard business school (“HBS”) questioning the current system of capitalism and how accounting should contribute to solve the issue through influencing our decision-making mechanism (emphasis mine).

Reimagining capitalism is an imperative. We need to create a more inclusive and sustainable form of capitalism that works for every person and the planet. Massive environmental damage, growing income and wealth disparity, stress, and depression within developed economies amid a substantial economic boom are examples of how our current system of creating and distributing value is broken. We need to be able to factor into our decision-making the consequences of our actions not only for financial and physical capital but also for human, social and natural capital. […]

In the absence of clearly defined impact metrics and transparency, these considerations are likely to be absent from decision-making. Decisions will continue to be made on existing financial metrics that do not reflect a holistic view of how an organization creates value as they ignore impacts on employees, customers, the environment and the broader society.

In order to provide actionable signals for business leaders, these impacts must be connected to accounting statements.

Even now, many corporations already release sustainability disclosures mostly within their sustainability reports or integrated reports. However, as the sustainability disclosures are separate from the financial statements, it is hard to see the connection between the two, and there is little influence on the decision-making of investors and management. Impact-weighted accounts are one clear example of how to solve the issue and help achieve the mission above. The HBS article continues:

Impact-weighted accounts are line items on a financial statement, such as an income statement or a balance sheet, which are added to supplement the statement of financial health and performance by reflecting a company’s positive and negative impacts on employees, customers, the environment and the broader society.

The aspiration is an integrated view of performance which allows investors and managers to make informed decisions based not only on monetized private gains or losses, but also on the broader impact a company has on society and the environment.

3. Example of Impact-Weighted Accounts Initiative (“IWAI”)

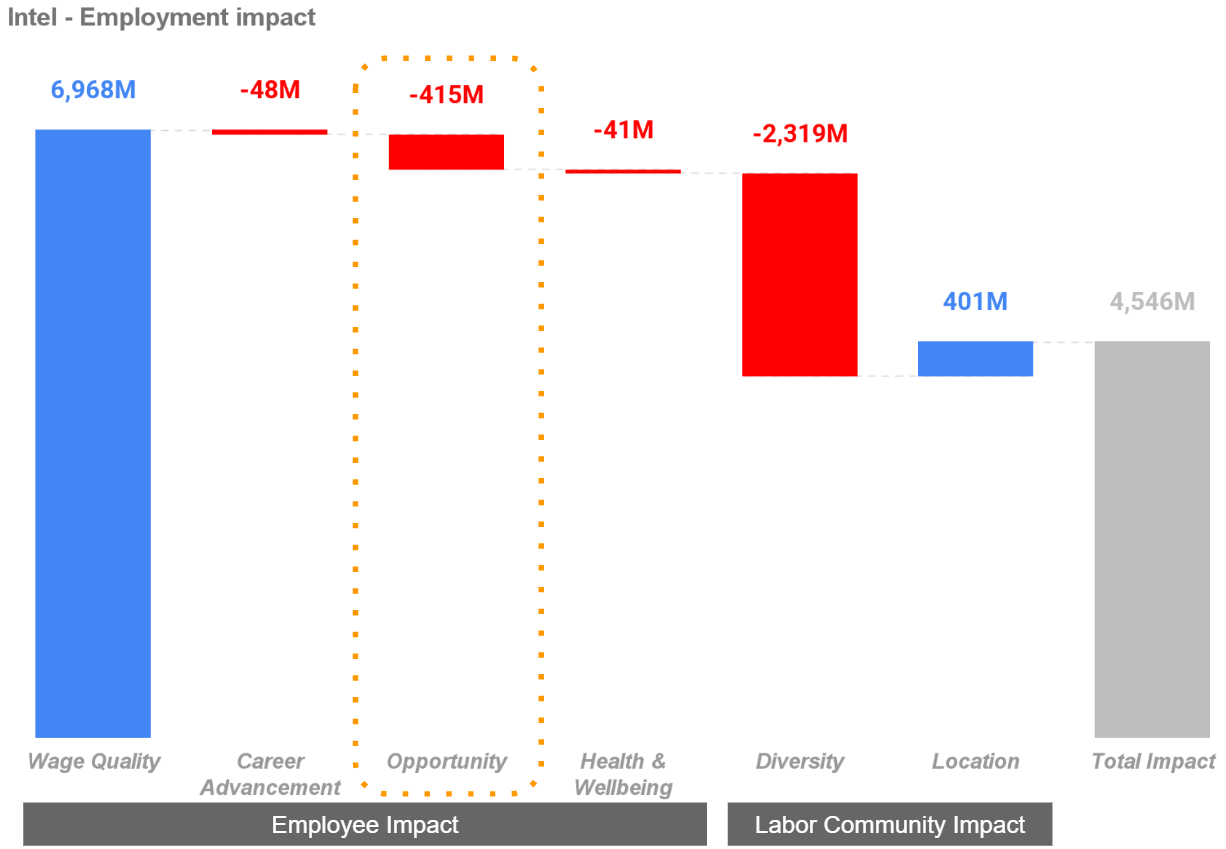

The Impact-Weighted Accounts Initiative (“IWAI”), built by Harvard Business School, has been used by large corporations such as Intel, SK, ACCIONA, Eisai, Daiichi-insurance and investors such as Blackrock and Calvert. Below is an example from Intel’s employment impact analysis. If you are interested in how each impact item is calculated, you can refer to the linked document.

Intel’s impact analysis (Accounting for Organizational Employment Impact, Harvard business school Accounting & Management Unit Working Paper (21-050) by David Freiberg et al.)

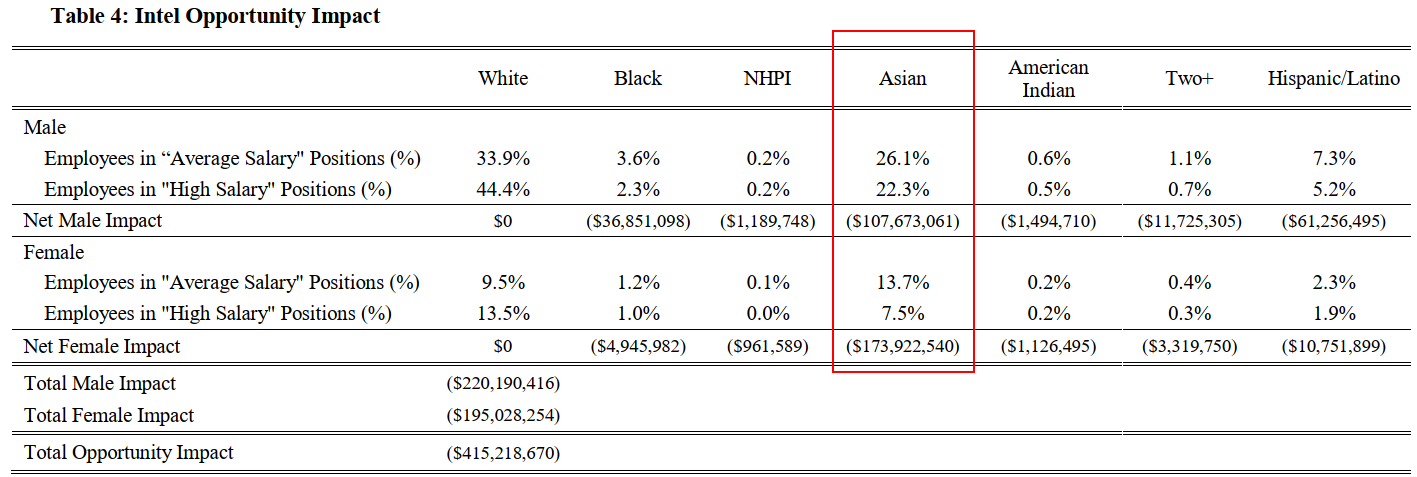

The table below describes the Opportunity impact for each gender-race/ethnicity group. The opportunity dimension monetizes the impact of unequal access to employment within an organization, using the “high salary” group to represent firm hierarchy. As such, a large (negative) opportunity impact describes a firm where minority group employees predominantly hold lower salaried positions.

All values represent negative impacts, as employees are negatively impacted by inequitable job category representation. Overall, the total opportunity impact for Intel is ($415 million). The largest individual negative impacts are driven by Asian females ($174 million) and Asian men ($108 million). Notably, while Black men represent only 3.4% of total employees at Intel, they bear 9% of the total opportunity impact (a negative impact of $37 million out of the total $415 million). Asian men, on the other hand, face a very large opportunity impact ($108 million, and 26% of the total impact) that is proportional to their overall representation in the workforce (25.6% of total employees). Asian women are only 12.6% of total employees at Intel but carry 42% of the negative opportunity impact.

Breakdown of the opportunity impact shown in the previous figure, from the same source.

4. Challenges and Recent Developments

One of the obvious challenges to enhance this new practice is ensuring comparability across companies. Unless all the companies you want to compare assess the same types of impacts, your comparison won’t be apples to apples. Moreover, business logic and the methods used for the measurement need to be consistent to do meaningful comparisons with peers. These are all relevant points for Gojo, a global group of companies that can be very different from each other. To tackle this issue, we already have internationally accepted and trusted standards for "traditional" accounting, such as IFRS and US GAAP. Now we need something similar for impact accounting. Once the international standards are there, external audits can be also done to assure accuracy.

Luckily, international organizations have already started working on this. Below are some recent developments and events related to global standards for impact accounts/disclosures. HBS and other institutions have also been publishing several research and case studies:

- November 2021: International Sustainability Standard Board (ISSB) was established under the IFRS foundation at COP26 in 2021 to deliver a comprehensive global baseline of sustainability-related disclosure standards.

- February 2022: Impact Economy Foundation launched Impact-Weighted Accounts Framework

- April 2022: ISSB delivered proposals that create a comprehensive global baseline of sustainability disclosures.

- Also April 2022: Impact task force (created in 2021 with the support of G7) urgently called for mandatory accounting for impact.

- 2022 Spring: Impact weighted accounts were introduced by a "New Capitalism" task force under the Japanese Government.

5. What Can Gojo Do About Impact Accounting?

We have recently completed a materiality analysis (a method to identify and prioritize the issues that are most important to an organization and its stakeholders, which helps companies with resource allocation, communication and long term thinking) through surveys done by several stakeholders and defined the top agenda for Gojo. One of the agenda items is client protection. Below are examples of ways to measure the impact of products which Gojo is considering.

- Affordability of products: Difference between the effective interest rate (“EIR”) of Gojo’s products and the industry average.

- Access to the underserved: # of underserved clients * Financial exclusion costs ($196.5 for consumer finance industry as per the HBS research.)

Although Gojo and its partners have a variety of impacts (both positive and negative), it is not practical to comprehensively measure and report all of them at this stage. Rather, we should start small, beginning with what is most important for stakeholders, then gradually expand our scope and improve the measurements. As far as I know, no microfinance institution and no Japanese startup has yet implemented impact-weighted accounting in practice. At Gojo, we're studying the issue and hope to become the first in both categories to advance to the next phase.

Ryo Satake is an accountant and works in Gojo's strategy and analytics team. He recently led the process of financial modelling for Gojo's overall business and has helped to formalise the budgeting and financial reporting processes for Gojo's partner companies.